One nation is accumulating gold as a weapon of financial sovereignty. The other is restricting imports to protect its economy. Together, China and India are rewriting the future of gold demand.

| Gold is no longer just a precious metal. In 2026, it has become a geopolitical asset, a monetary hedge, and a symbol of economic power. While most investors focus on price charts, the real story is happening behind the scenes. China’s central bank has quietly increased its gold reserves to 2,308 tonnes, extending an 18-month buying streak. Meanwhile, India traditionally the world’s largest consumer of gold jewellery—is actively discouraging physical imports as prices soar past ₹1.56 lakh per 10 grams. This is not a coincidence. It is a strategic divergence. One country is buying gold to reduce dependence on the U.S. dollar. The other is limiting gold inflows to defend its currency and trade balance. The implications stretch far beyond Beijing and New Delhi. They could shape the next decade of global gold prices. |

The Gold Divide at a Glance

| China | India |

| 2,308 tonnes in reserves | Import restrictions tightened |

| 18 consecutive months of buying | Jewellery demand down 16% |

| US$6.2B ETF inflows in January 2026 | Gold above ₹1.56 lakh/10g |

| De-dollarization strategy | Forex conservation strategy |

| Gold as sovereign power | Gold as managed economic asset |

The Message Is Clear

China is accumulating. India is regulating. And global investors are paying attention.

Why China Is Buying Gold Heavily

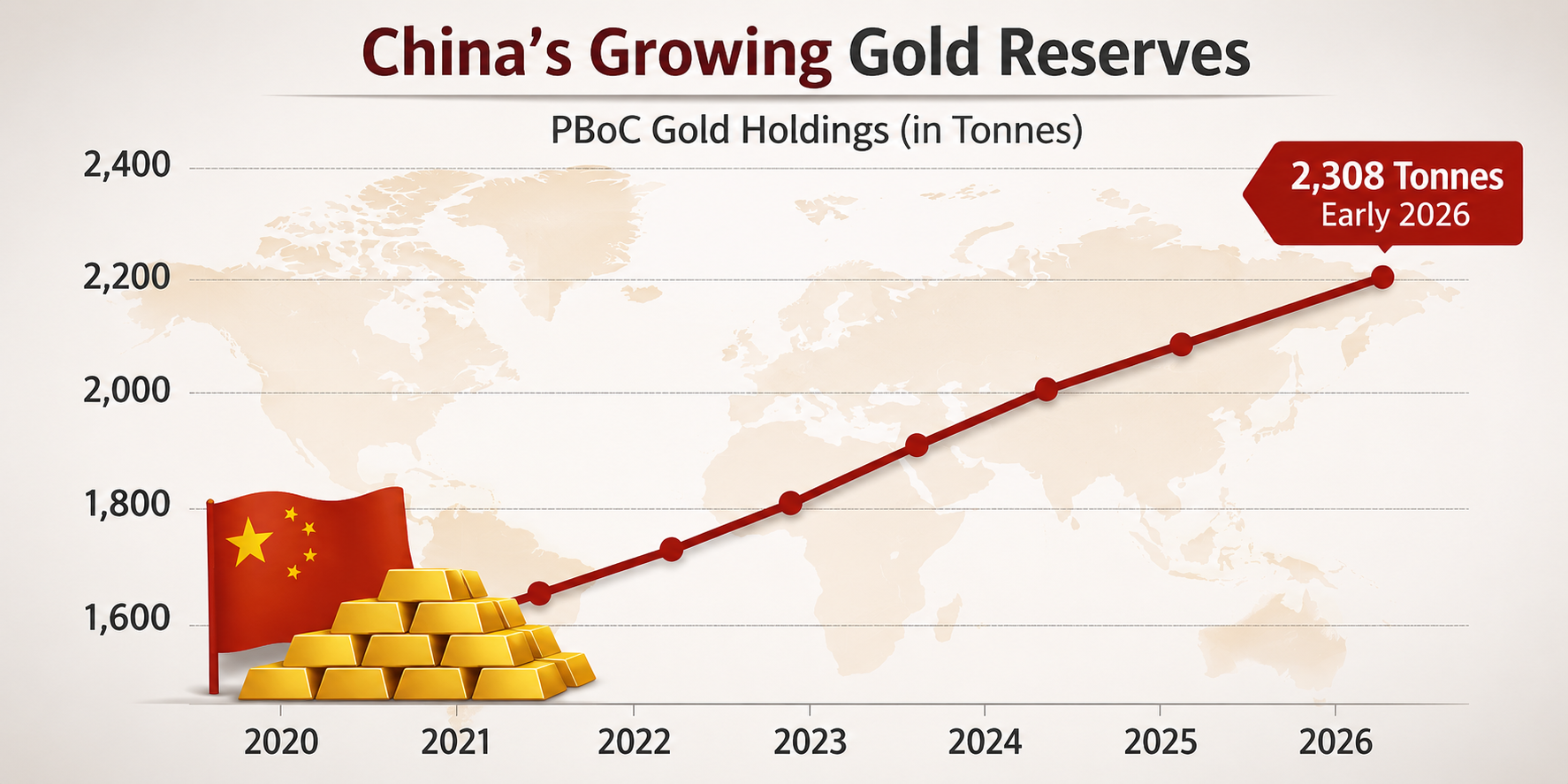

China’s central bank has been adding gold for 18 consecutive months, reaching 2,308 tonnes by early 2026. This surge is not speculative — it’s strategic.

Key Drivers:

- De-dollarization: Reducing dependence on the U.S. dollar and insulating reserves from sanctions.

- Geopolitical hedging: Gold offers neutrality in global trade and protection against financial weaponization.

The De-Dollarization Playbook

Every major geopolitical conflict over the last decade has reinforced one lesson:

Countries that rely too heavily on foreign reserve currencies face strategic vulnerabilities.

Gold solves this problem.

Unlike currencies:

- Gold cannot be printed.

- Gold cannot be sanctioned.

- Gold cannot be frozen by foreign governments.

- Gold remains universally accepted.

For China, every additional tonne strengthens economic independence.

The Reserve Race Nobody Is Talking About

While retail investors debate whether gold is expensive, central banks continue buying.

China’s reserves have risen from approximately 1,800 tonnes in 2020 to 2,308 tonnes in 2026. That’s not speculative demand. That’s sovereign demand.

And sovereign demand rarely chases short-term profits.

Investor Confidence Is Following

Chinese investors are mirroring the government’s confidence.

Gold ETFs attracted approximately US$6.2 billion in inflows during January 2026 alone.

The reason?

Investors increasingly view gold as protection against:

- Currency instability

- Global debt expansion

- Market volatility

- Geopolitical uncertainty

When central banks become the largest buyers in the market, gold stops behaving like a luxury product and starts behaving like a strategic reserve asset.

That changes everything.

Source: https://www.pbc.gov.cn/

Why India Is Holding Back

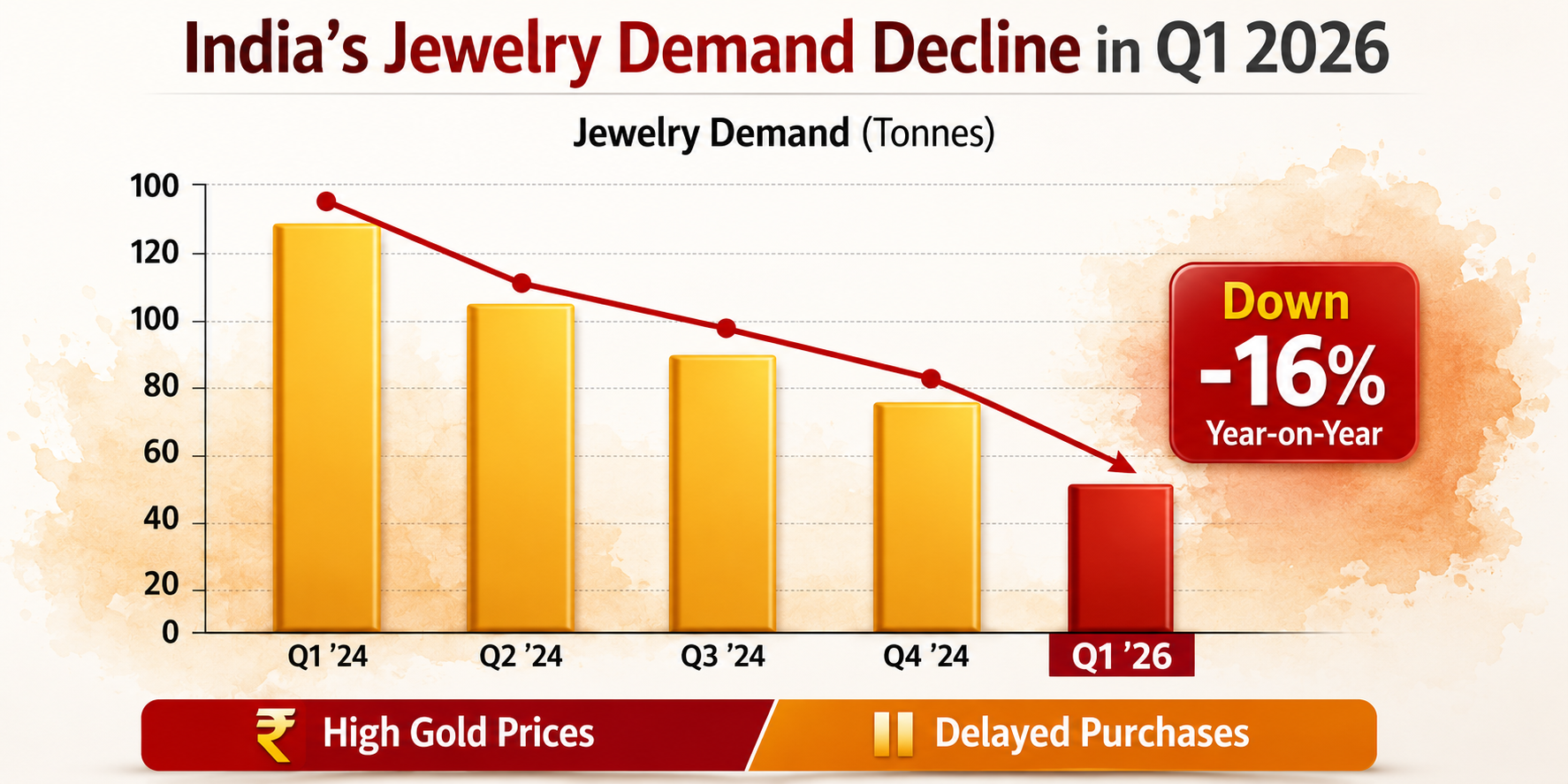

India, traditionally the world’s largest consumer of gold jewelry, is showing restraint. Jewelry demand fell 16% in Q1 2026, as prices crossed ₹1.56 lakh per 10g. The government responded with import restrictions and higher duties to protect foreign exchange reserves.

Key Factors:

- Price sensitivity: Indian households delay purchases when prices spike.

- Policy defense: Import curbs to stabilize the rupee and reduce trade deficits.

- Financialization: Shift toward Sovereign Gold Bonds (SGBs) and ETFs instead of physical bullion.

The Price Shock Effect

As prices crossed ₹1.56 lakh per 10 grams, households began delaying purchases.

Jewellery demand declined approximately 16% in Q1 2026. This is classic Indian consumer behavior. Demand doesn’t disappear. It pauses.

Protecting the Rupee

India imports most of the gold it consumes.

Large imports create pressure on:

- Foreign exchange reserves

- Current account deficits

- Rupee stability

To reduce these pressures, policymakers have tightened controls and maintained higher import duties. The objective isn’t to stop gold ownership.

The objective is to manage economic risk.

The Rise of Financial Gold

Something more important is happening beneath the surface.

Indian investors are slowly shifting from:

❌ Jewellery

❌ Physical bullion

towards

✅ Gold ETFs

✅ Sovereign Gold Bonds

✅ Digital Gold

✅ Gold SIPs

India isn’t abandoning gold.

India is digitizing gold.

The Global Gold Divide

The contrast between China and India reveals a historic shift.

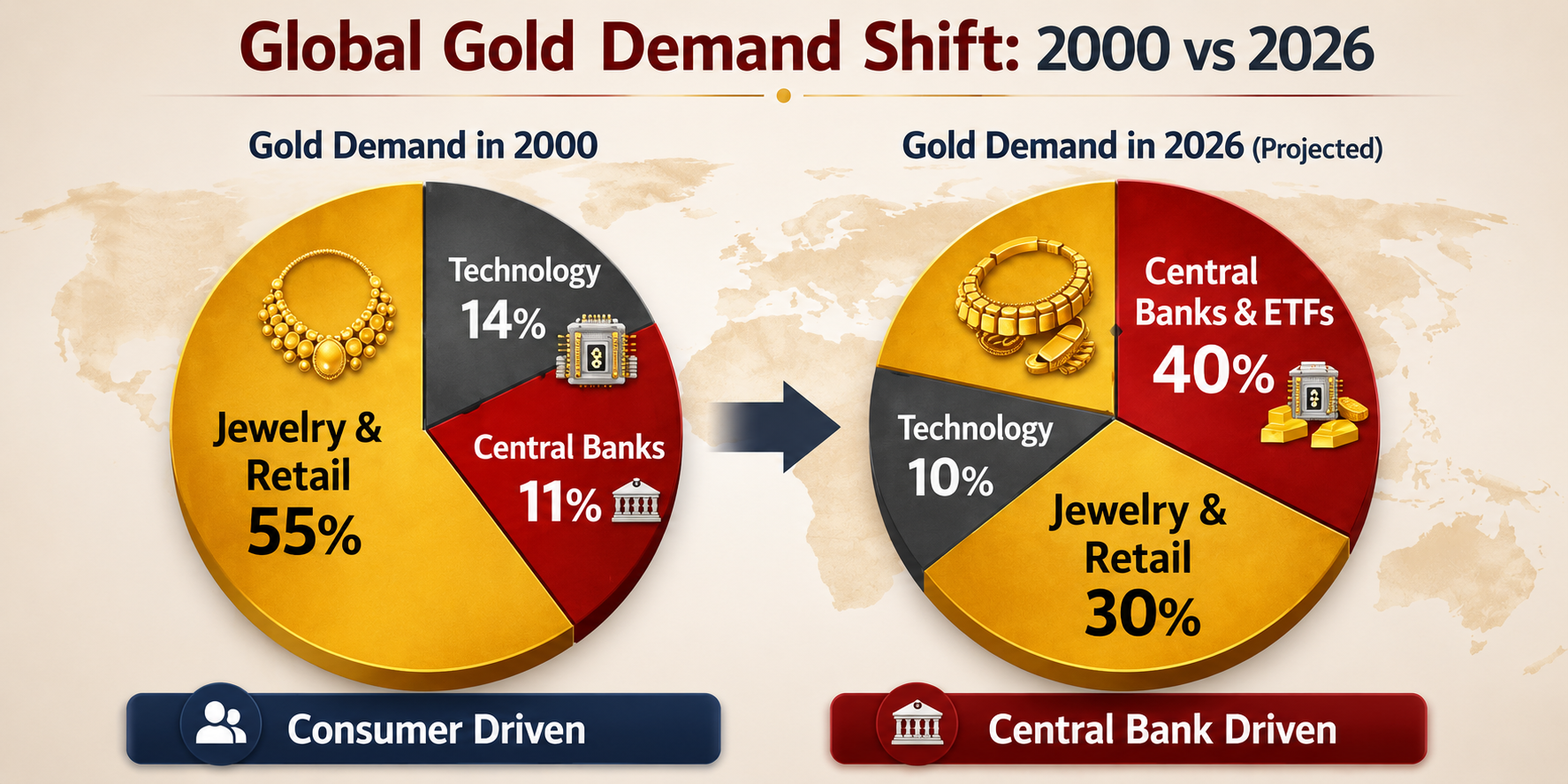

For decades, gold demand was driven by consumers.

Today, gold demand is increasingly driven by governments.

Then vs Now

| Gold Demand in 2000 | Gold Demand in 2026 |

| Jewellery & Retail: 55% | Central Banks & ETFs: 40% |

| Technology: 14% | Jewellery & Retail: 30% |

| Central Banks: 11% | Technology: 10% |

The market has fundamentally changed.

Gold demand is moving from consumer-driven to institution-driven.

What This Means for Investors

Gold’s Floor Is Rising

Central banks don’t buy gold for six months. They buy for decades. This creates structural demand that helps support prices.

Volatility May Decline

When official institutions become major buyers, panic selloffs tend to have stronger support levels.

Digital Gold Wins

The future investor wants:

- Fractional ownership

- Instant liquidity

- SIP investing

- Mobile-first access

This is one reason digital gold adoption continues to accelerate.

The Biggest Takeaway

The gold market is no longer asking: “Will consumers buy more jewellery?”

The market is now asking: “How much gold will central banks buy next?”

That is a profound shift.

What Happens Next?

The next decade will likely create two distinct gold stories.

For Nations

Gold becomes:

- A reserve asset

- A hedge against geopolitical fragmentation

- A tool of monetary independence

For Individuals

Gold becomes:

- More digital

- More accessible

- More systematic through SIP investing

The transformation has already begun.

Frequently Asked Questions

1. Why is China buying so much gold?

China is reducing dependence on the U.S. dollar while strengthening financial sovereignty through reserve diversification.

2. Why are Indians buying less jewellery?

Record-high prices have caused households to postpone purchases, leading to lower short-term demand.

3. Does weaker jewellery demand mean gold prices will fall?

Not necessarily. Central bank purchases and ETF inflows are increasingly replacing jewellery demand as the dominant market driver.

4. Is digital gold becoming mainstream?

Yes. Investors increasingly prefer convenience, liquidity, and SIP-based investing over traditional ownership models.

5. Could central bank buying keep gold prices elevated?

Historically, sustained central bank accumulation creates long-term structural support for gold prices.

Gold’s biggest transformation is not happening in jewellery stores. It is happening in central bank vaults.China is buying gold to strengthen sovereignty. India is managing gold to protect stability. Together, they reveal the future of the gold market.

Gold is no longer just wealth.

Gold is strategy.

Gold is power.

Gfolio Research Desk

Helping investors understand the forces shaping the future of gold, silver, and digital wealth.